Introduction

High Risk Personal Loans Guaranteed Approval Direct Lenders, represent a unique segment of the lending market, characterized by their appeal to individuals with suboptimal credit scores or precarious financial histories. Unlike traditional loans, high-risk personal loans cater to borrowers who may face difficulties securing credit through conventional channels.

Despite the higher interest rates and more stringent repayment terms associated with these loans, they remain a vital financial tool for many. In today’s complex financial landscape, a significant number of individuals encounter barriers when attempting to access credit.

Factors such as past bankruptcy, high debt-to-income ratios, or poor credit scores can severely limit borrowing options. High-risk personal loans emerge as an alternative for those in need of immediate funds, offering an opportunity to manage unexpected expenses, consolidate debt, or finance essential purchases.

Also Read: What is a Cup Loan Program: Real or Fack

Overview

The concept of guaranteed approval from direct lenders adds another layer of appeal to high-risk personal loans. Direct lenders streamline the borrowing process by eliminating intermediaries, which can result in faster approvals and more personalized service.

For borrowers who may have been turned away by traditional lenders, the promise of guaranteed approval presents a viable path to securing necessary funds.

This blog post will delve into the intricacies of high-risk personal loans, providing a comprehensive overview of their advantages, potential pitfalls, and the critical role direct lenders play in this niche market. By understanding the dynamics at play, borrowers can make informed decisions and navigate the complexities of high-risk lending with greater confidence.

What is a High-Risk Personal Loan?

A high-risk personal loan is a type of loan extended to individuals who present a higher level of risk to the lender, often due to factors such as poor credit history, lack of income verification, or other financial challenges.

These loans are characterized by higher interest rates and less favorable terms compared to conventional loans, reflecting the increased risk the lender assumes by providing the loan.

Several Factors to Loan as High-Risk

One primary factor is a poor credit history. Borrowers with a history of missed payments, defaults, or bankruptcies are considered high-risk because their past behavior indicates a likelihood of future financial difficulties. Another significant factor is the lack of income verification.

Traditional lenders typically require proof of stable and sufficient income before approving a loan application. In contrast, high-risk personal loans may be offered to individuals without such documentation, increasing the lender’s risk.

High-interest rates are another hallmark of high-risk personal loans. To compensate for the elevated risk, lenders charge substantially higher interest rates than those associated with standard loans. This ensures that the lender can still achieve a return on investment even if some borrowers default.

Typical profiles of borrowers who might seek high-risk personal loans include those with low credit scores, inconsistent employment history, or recent financial setbacks. These individuals often find it challenging to secure financing through traditional means due to their perceived inability to repay the loan.

Traditional Lenders

Traditional lenders, such as banks and credit unions, generally deny loan applications from high-risk individuals to mitigate potential losses. Consequently, these borrowers turn to direct lenders specializing in high-risk personal loans, who are more willing to assume the associated risks in exchange for higher returns.

Understanding the nature of high-risk personal loans is crucial for potential borrowers and lenders alike. While these loans provide essential financial access to those in need, they also come with significant costs and risks that must be carefully considered.

Types of High-Risk Personal Loans

High-risk personal loans cater to individuals with less than stellar credit or unstable financial histories. These loans often come with higher interest rates and more stringent terms to offset the risk to lenders. Below are some common types of high-risk personal loans, each with unique features, requirements, and use cases.

No Income Verification Loans

As the name suggests, no income verification loans do not require borrowers to provide proof of income. This type of loan is particularly beneficial for self-employed individuals or those with irregular income streams.

Despite the flexibility, these loans generally come with higher interest rates and may demand collateral to mitigate the lender’s risk. Typical use cases include urgent medical expenses, home repairs, or consolidating high-interest debt.

No Credit Check Loans

No credit check loans are designed for individuals with poor or nonexistent credit histories. Lenders offering these loans do not conduct traditional credit checks, making them accessible to a broader range of borrowers.

However, the absence of a credit check usually results in elevated interest rates and shorter repayment terms. These loans are often used for emergency expenses, such as car repairs or unexpected bills, where quick access to funds is crucial.

Payday Loans

Payday loans are short–term, high–interest loans typically due on the borrower’s next payday. These loans are easily accessible and do not require a credit check, making them a popular option for individuals facing immediate financial needs.

However, the high interest rates and short repayment periods can lead to a cycle of debt if not managed responsibly. Payday loans are commonly used for small, urgent expenses like utility bills or minor medical costs.

Title Loans

Title loans require borrowers to use their vehicle as collateral. The loan amount is usually a percentage of the vehicle’s value, and the lender holds the title until the loan is repaid.

These loans are accessible to individuals with poor credit but come with the risk of losing the vehicle if the loan is not repaid. Title loans are often used for larger, immediate financial needs, such as significant home repairs or medical emergencies.

Each type of high-risk personal loan serves different needs and comes with its own set of advantages and disadvantages. Understanding the unique features and requirements of these loans can help borrowers make informed decisions that best suit their financial situations.

How Can You Get a High-Risk Personal Loan?

Obtaining a high-risk personal loan involves a series of essential steps, each designed to enhance your chances of securing the loan successfully. The process begins with thorough research and identification of suitable lenders.

STEP- 1

Not all lenders are willing to offer high-risk personal loans, so focusing on direct lenders who specialize in this area is crucial. Online platforms and financial forums can serve as valuable resources in finding reputable lenders who provide guaranteed approval for high-risk personal loans.

STEP- 2

Once a list of potential lenders is compiled, the next step is to prepare all necessary documentation. Commonly required documents include proof of income, bank statements, identification, and sometimes collateral information.

STEP- 3

Ensuring that all paperwork is current and accurate can significantly improve the likelihood of approval. Additionally, having a clear understanding of your credit report and being prepared to explain any discrepancies or negative marks can be beneficial.

STEP- 4

The application process for high-risk personal loans often involves filling out detailed forms either online or in person. It’s important to provide honest and complete information on these applications to avoid any potential issues down the line.

Many direct lenders offering guaranteed approval may also conduct a credit check and verify your employment status, so being transparent is crucial.

STEP- 5

Improving your chances of approval can also involve taking proactive steps such as reducing existing debt, increasing your income, or securing a co-signer. These actions demonstrate financial responsibility and can make you a more attractive candidate to lenders.

Additionally, maintaining open communication with the lender throughout the process can provide clarity and help address any concerns they may have.

STEP- 6

Finally, understanding the terms and conditions of the loan agreement before signing is paramount. This includes the interest rate, repayment schedule, and any associated fees. Thoroughly reviewing these details ensures that you are fully aware of your obligations and can manage the loan responsibly.

By following these steps, you can navigate the complexities of securing a high-risk personal loan more effectively.

Top Direct Lenders for High-Risk Personal Loans

When it comes to securing high-risk personal loans, selecting the right direct lender is crucial. Several lenders specialize in providing these loans, ensuring that individuals with less-than-stellar credit histories have access to financial support. Among these lenders, ‘CashUSA‘ and ‘OppLoans‘ stand out due to their unique offerings and customer-centric approaches.

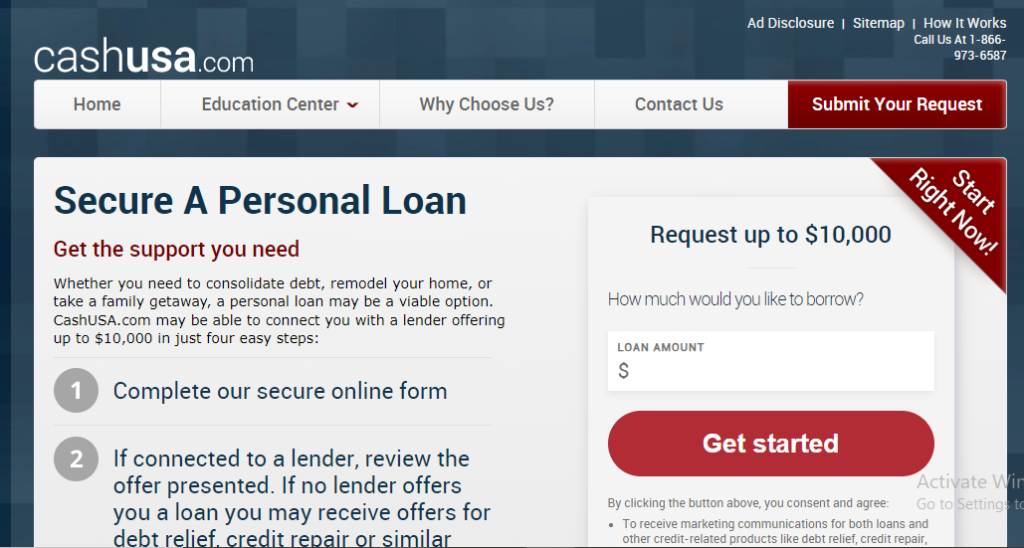

CashUSA

CashUSA is a prominent player in the high-risk loan market. Known for its swift approval process and minimal credit requirements, CashUSA connects borrowers with a network of lenders. This platform is particularly user-friendly, offering loans ranging from $500 to $10,000.

Customer reviews often highlight the ease of application and the transparency of terms and conditions. Special features include educational resources aimed at improving financial literacy, which can be especially beneficial for those looking to rebuild their credit.

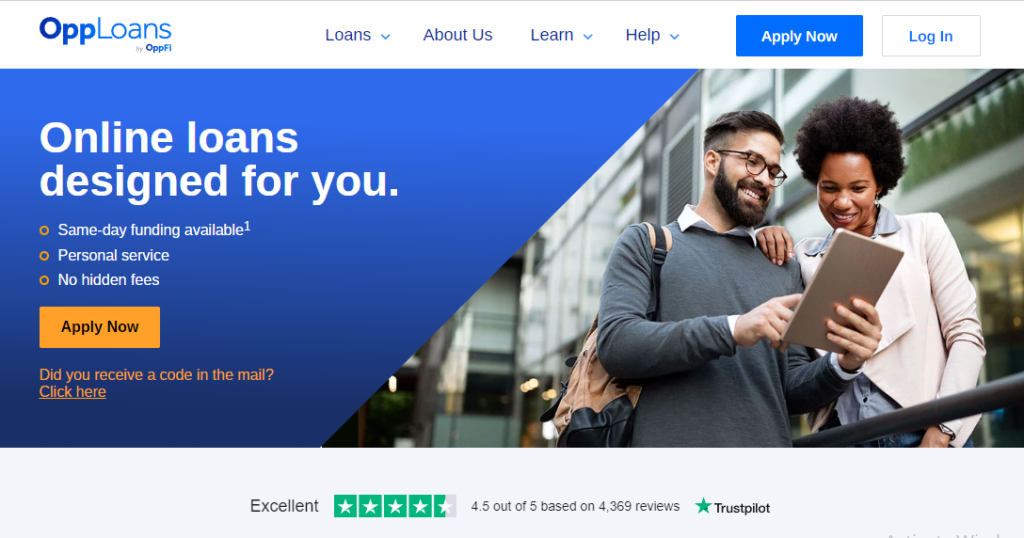

OppLoans

OppLoans is another reputable lender catering to high-risk borrowers. What sets OppLoans apart is its focus on customer service and flexible repayment terms. They offer loans up to $4,000 with a straightforward application process.

OppLoans is highly rated for its personalized customer support, which ensures that borrowers fully understand their loan agreements. Additionally, OppLoans reports to all three major credit bureaus, helping borrowers improve their credit scores through timely repayments.

Other Notable Lenders

Other notable lenders in this space include NetCredit and OneMain Financial. NetCredit offers personal loans up to $10,000, with a strong emphasis on transparency and no hidden fees. Their ‘My Credit Builder’ program is a unique feature designed to help borrowers enhance their credit scores.

OneMain Financial, on the other hand, provides loans up to $20,000 and is known for its in-person consultations, which can be advantageous for those who prefer face-to-face interactions.

Choosing the right lender involves considering various factors such as loan amounts, interest rates, repayment terms, and customer service. By reviewing the unique offerings and customer feedback of each lender, borrowers can make informed decisions that best meet their financial needs.

Pros and Cons of High-Risk Personal Loans

High-risk personal loans, often marketed with the promise of guaranteed approval from direct lenders, present both advantages and disadvantages that potential borrowers must consider carefully. On the positive side, one of the most notable benefits is the quick access to funds.

These loans can be a lifeline for individuals facing urgent financial needs, such as medical emergencies or unexpected expenses, as the approval process is typically expedited compared to traditional loans.

Another significant advantage is the opportunity to improve credit scores. For borrowers with a poor credit history, timely repayments on a high-risk personal loan can demonstrate financial responsibility and positively impact their credit profile.

This can open the door to better borrowing terms in the future, as a higher credit score may lead to lower interest rates and more favorable loan conditions.

Despite these Benefits

High-risk personal loans come with considerable drawbacks. The most prominent disadvantage is the high-interest rates associated with these loans. To compensate for the increased risk of lending to individuals with poor credit, lenders often charge significantly higher interest rates.

This can lead to substantial long-term costs and make the loan more expensive than initially anticipated. Additionally, there is the potential for debt traps.

Borrowers who struggle to meet the stringent repayment terms may find themselves needing to take out additional loans to cover existing debts, leading to a cycle of borrowing that can be difficult to break. This situation can be exacerbated by the often rigid repayment schedules, which may not offer much flexibility for those facing financial instability.

In conclusion, while high-risk personal loans can provide immediate financial relief and a chance to rebuild credit, they also carry the risk of high costs and potential debt cycles. Prospective borrowers should weigh these factors carefully and consider their long-term financial health before committing to such a loan.

Easy Personal Loans You Can Get

When high-risk personal loans are not a viable option, several alternative lending options, such as auto title loans, payday loans, and pawnshop loans, can provide quick financial relief. Each of these loans operates under different mechanisms and comes with its own set of requirements, interest rates, and risks.

Auto Title Loans

Auto title loans involve borrowing money against the equity of your vehicle. To qualify, you must own a car that is paid off or has significant equity. The lender retains the car title until the loan is repaid. The loan amount is typically a percentage of the car’s value, often ranging from 25% to 50%.

Interest rates on auto title loans can be extremely high, sometimes reaching triple-digit APRs. The primary risk is the potential loss of your vehicle if you fail to repay the loan on time.

Payday Loans

Payday loans are short-term, high-interest loans intended to cover immediate expenses until your next paycheck. To qualify, you generally need proof of income, a bank account, and identification. Payday loans are typically small, ranging from $100 to $1,000, and must be repaid within a few weeks.

Interest rates can be exorbitant, often exceeding 400% APR. The risk lies in the short repayment period and high fees, which can trap borrowers in a cycle of debt if they cannot repay the loan promptly.

Pawnshop Loans

Pawnshop loans involve using personal items of value, such as jewelry or electronics, as collateral. The pawnshop appraises the item and offers a loan based on its value. The loan amount is usually a fraction of the item’s worth, and interest rates can vary but are generally steep.

If you fail to repay the loan within the agreed period, the pawnshop keeps the item and sells it to recover the loan amount. The risk here is the loss of personal valuables if the loan is not repaid.

These alternative loans offer immediate access to funds but come with significant risks and high costs. Borrowers should carefully consider their ability to repay and explore all available options before committing to any of these lending solutions.

Conclusion

In navigating the intricate landscape of high-risk personal loans, it is paramount to understand the multifaceted aspects involved in securing such financial assistance. High-risk personal loans, often sought from guaranteed approval direct lenders, provide a vital lifeline for individuals with precarious credit histories or pressing financial needs.

However, these loans come with their own set of challenges and risks, which must be meticulously weighed.Moreover, it is crucial to recognize that not all lenders operate with the same level of transparency and ethical standards.

Due diligence in researching potential lenders and carefully scrutinizing loan terms can mitigate the risks of falling prey to predatory lending practices. Utilizing resources such as financial reviews, customer testimonials, and expert advice can provide invaluable insights.

By thoroughly understanding the nuances of high-risk personal loans and weighing all available options, borrowers can navigate this complex terrain more effectively, making choices that safeguard their financial stability and future well-being.

Frequently Asked Questions

Can I get a High Risk Personal Loans Guaranteed Approval Direct Lenders?

Although several lenders focus on providing loans to borrowers with poor credit or high-risk profiles, it’s crucial to remember that not all borrowers will receive a guaranteed approval. Since every lender has different requirements and methods of evaluation, approval will depend on a number of variables.

How can I improve my chances of getting approved for a high-risk personal loan?

You can raise your credit score, find a cosigner with good credit, or provide collateral to increase your chances of being approved for a high-risk personal loan. You can also improve your chances of acceptance by providing evidence of consistent income and a track record of good financial management.

What is considered a high-risk personal loan?

A loan given to someone who has a bad credit history, little income, or other characteristics that raise the lender’s perceived risk is usually referred to as a high-risk personal loan. When opposed to loans given to borrowers with stronger credit, these loans frequently have stricter terms and higher interest rates.

Are high-risk personal loans a good solution for bad credit borrowers?

When it comes to financing, high-risk personal loans can be an option for applicants with poor credit. But it’s crucial to pay close attention to the conditions and costs connected to these loans. Before moving further, it’s critical to determine your ability to repay the loan because they frequently have higher interest rates and costs.